%20(4).png)

![[background image] image of cityscape background (for an architect firm)](https://cdn.prod.website-files.com/68961ade6feff9cbdffc080d/69384e066e0e9a310b6817f8_061f6bac-48bf-44b8-a689-078dacd8009f.avif)

TL;DR:

- Property financing involves understanding loan types, interest rate structures, and total costs to determine what you can afford. Different loan options like conventional, FHA, VA, and USDA have varying down payment and credit requirements, affecting your initial costs and eligibility. Budgeting for closing costs, reserves, and potential repairs is crucial, with the entire mortgage process typically taking 30 to 60 days from application to closing.

Most people assume property financing is just picking a mortgage and signing paperwork. That assumption costs families thousands of dollars. Explaining property financing properly means going beyond the basic loan definition to show you how loan types, interest rate structures, and total upfront costs interact to shape what you can actually afford. Whether you are buying your first home or stepping up to something larger, the decisions you make in the financing stage will follow you for 15 to 30 years. This article gives you a clear, honest picture of how all the pieces fit together.

| Point | Details |

|---|---|

| Loan type changes your down payment | FHA, VA, and USDA loans each carry different down payment and credit score requirements that affect who qualifies. |

| Fixed rates mean payment certainty | A fixed-rate mortgage protects you from rising rates and makes monthly budgeting predictable over the full loan term. |

| Closing costs are often underestimated | Budget an additional 2% to 5% of the purchase price on top of your down payment for lender fees and title costs. |

| Pre-approval outranks pre-qualification | Sellers treat pre-approval as a serious offer signal because it involves actual lender verification of your finances. |

| Rate shopping has a time window | Comparing multiple lenders within a 45-day period counts as a single credit inquiry, protecting your credit score. |

Understanding property loans starts with recognizing that not all mortgages are created equal. The loan category you land in affects your down payment, monthly cost, credit requirements, and long-term risk. Most buyers have four main categories to consider.

Conventional loans are not backed by any government agency. Lenders set their own standards, which typically means stricter credit requirements and a down payment of 3% to 5% for first-time buyers. If your down payment falls below 20%, you will pay private mortgage insurance (PMI) each month until you reach that equity threshold. PMI adds anywhere from 0.5% to 1.5% of the loan amount per year to your costs.

Government-backed loans exist specifically to help buyers who may not qualify for conventional financing:

Here is a quick comparison of how these property financing options stack up:

| Loan type | Minimum down payment | Credit score minimum | PMI required |

|---|---|---|---|

| Conventional | 3% to 5% | 620 (typical) | Yes, if under 20% down |

| FHA | 3.5% | 580 | Yes (for life of loan) |

| VA | 0% | Varies by lender | No |

| USDA | 0% | 640 (typical) | No (guarantee fee instead) |

Investment property loans sit in a separate category entirely. Lenders treat them as higher risk, so expect down payment requirements of 15% to 25% and higher interest rates than you would see on a primary residence loan. If you are exploring ways to finance a home specifically for investment purposes, plan your numbers conservatively.

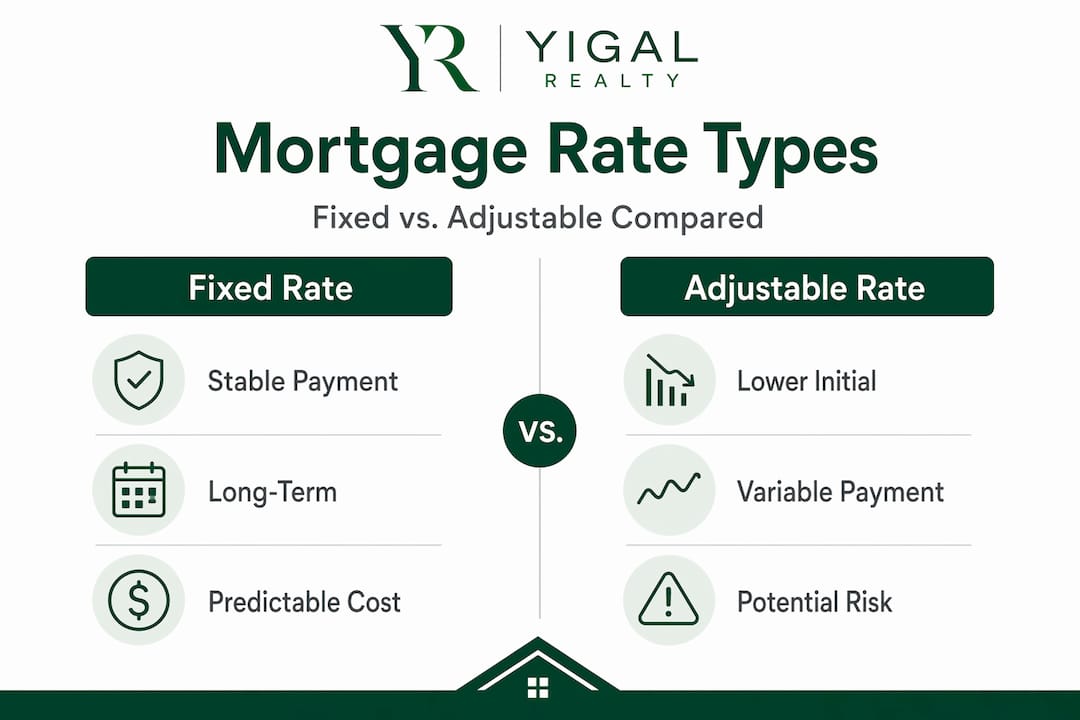

Property mortgage explained simply: the interest rate structure you choose determines how much your payment can change over time. This is not a small detail. It is one of the biggest risk factors in property financing.

Fixed-rate mortgages lock in your interest rate for the entire loan term, whether that is 15 or 30 years. Your principal and interest payment never moves. Fixed-rate mortgages provide stability that protects you against inflation and rising interest rate environments, which is especially valuable when rates are low at origination. The tradeoff is that your starting rate will typically be slightly higher than the initial rate on an adjustable product.

Adjustable-rate mortgages (ARMs) start with a fixed introductory period, usually 5, 7, or 10 years, then adjust annually based on a market index. The starting rate is lower, which reduces your early payments. However, ARMs carry a risk of payment shock of 8% to 37% after the introductory period ends depending on how much rates have moved.

ARMs come with cap structures that limit how much your rate can move. A common structure is a 2/2/5 cap, which means:

That last number is the one most buyers ignore. If your starting rate is 5.5%, a worst-case scenario puts you at 10.5%. Run that number through a mortgage calculator before you sign.

A 0.5% rate increase can meaningfully raise your monthly payment and reduce your qualifying purchase price. Model at least three rate scenarios when evaluating any loan: your starting rate, your rate plus 2%, and your worst-case cap. If the worst case breaks your budget, an ARM is not the right product for your situation.

ARMs work well for buyers who are confident they will sell or refinance before or shortly after the initial fixed period ends. If you expect to move in five years and take a 7-year ARM, you capture the lower rate without ever facing the adjustment risk.

Pro Tip: When comparing a fixed-rate and an ARM offer, calculate the total interest paid over the period you actually plan to stay in the home. The ARM often wins in the short term but loses badly if your plans change and you stay longer.

Here is where many buyers get into real trouble. They save the down payment, get approved, and then discover a pile of additional costs they never planned for.

Closing costs typically range from 2% to 5% of the home’s purchase price. On a $400,000 home, that is $8,000 to $20,000 on top of your down payment. These costs cover appraisal fees, title insurance, lender origination fees, prepaid homeowner’s insurance, and several months of property taxes due at closing.

Many buyers underestimate total cash needed upfront, which includes closing costs, moving expenses, and cash reserves that lenders often require you to keep in the bank even after closing. A complete budget for your home purchase should include these four layers:

“Planning for a mortgage payment under 28% of gross income and total debt under 36% to 43% is traditional, but stress-testing your budget for job loss or a rate increase is what separates buyers who thrive from buyers who struggle.”

Pro Tip: Use a “high-water mark” budgeting method: take the highest possible monthly payment your loan allows (using the worst-case ARM cap or a rate increase scenario) and treat that as your baseline. If you can afford that number, every outcome below it is manageable.

For buyers dealing with variable income or adjustable payments, a sinking fund dedicated to mortgage fluctuations works well. Set aside a small fixed amount each month into a separate account. When payments increase, you draw from that fund rather than scrambling to cover the gap. You can get detailed guidance on financial planning for buyers covering how to structure these reserves effectively.

The real estate financing guide most people actually need is a clear picture of the process timeline. Here is how it typically runs:

The single most common cause of delays is slow borrower responses to document requests. Responding to lender requests within 24 hours keeps your file moving and protects your closing date. Avoid making large purchases, opening new credit accounts, or changing jobs during this period. Any change to your financial profile can trigger a new round of underwriting.

I have seen a pattern repeat itself constantly. Buyers get pre-approved for a certain amount and treat that number as their target instead of their ceiling. The bank’s approval reflects what you can technically borrow. It does not account for your actual lifestyle, your job security, or the maintenance costs of the home itself.

Borrowing at the absolute limit of your approval is one of the most financially fragile positions you can put your family in. One job change, one medical bill, or one bad year can turn a manageable mortgage into a crisis.

What I have found actually works is building your budget from the monthly payment you are comfortable with, then working backward to determine the purchase price. Not the other way around. The number the bank hands you should be a reference point, not a goal.

Shopping multiple lenders is also something buyers skip because they assume it hurts their credit. Shopping lenders within 45 days counts as a single inquiry. You owe it to yourself to get at least three Loan Estimates. Comparing only interest rates when choosing loans is another costly mistake. Always review the full APR and all closing costs on each Loan Estimate before deciding.

— Spiros

Understanding how to finance property is one thing. Applying that knowledge to an actual purchase, with real timelines, real lenders, and real costs, is where most buyers need support. Yigal-realty works directly with families and individuals at every stage of the home purchase process, from initial financing education to closing guidance.

The Yigal-realty team provides personalized support for buyers exploring the Israeli real estate market, including detailed breakdowns of local costs, payment structures, and project-specific financing options. If you are weighing property financing methods for a purchase in Beit Shemesh or surrounding communities, the resources available through Yigal-realty give you a meaningful starting point. Visit info.yigal-realty.com to explore current projects, connect with an agent, and access guides built specifically for buyers navigating this market.

Pre-qualification is a quick estimate based on self-reported data, while pre-approval involves full lender verification of income, credit, and assets. Pre-approval letters are valid for 60 to 90 days and carry far more weight with sellers.

Plan for an additional 2% to 5% in closing costs plus two to six months of mortgage payments in cash reserves, and at least 1% of the home’s value for immediate post-purchase expenses.

Fixed-rate mortgages suit buyers who plan to stay long term and want payment stability. ARMs work for buyers who are confident they will sell or refinance before the adjustment period begins, allowing them to benefit from the lower initial rate.

The full mortgage process from application to closing takes 30 to 60 days on average. Appraisal alone takes 10 to 16 days, and underwriting adds two to three more weeks.

No. Comparing lenders within 45 days is treated as a single credit inquiry by the major credit bureaus, so you can gather multiple Loan Estimates without damaging your score.