%20(4).png)

![[background image] image of cityscape background (for an architect firm)](https://cdn.prod.website-files.com/68961ade6feff9cbdffc080d/69384e066e0e9a310b6817f8_061f6bac-48bf-44b8-a689-078dacd8009f.avif)

TL;DR:

- Property appreciation is a powerful, compound growth mechanism that enhances wealth through market-driven and owner-driven factors.

- Investors benefit from leverage, equity acceleration, and long-term appreciation, but should always consider market cycles and real value growth.

Property appreciation is defined as the increase in a property’s market value over time, and it is one of the most powerful wealth-building mechanisms available to real estate investors. According to the Zillow Home Value Index, homes have increased in value by an average of 4.5% per year since 2001. On a $200,000 property, that translates to roughly $9,100 in added value every year without lifting a finger. Understanding why consider property appreciation is not optional for serious investors. It is the difference between treating real estate as a passive store of value and actively building generational wealth through it. The reasons for investing in property go well beyond rental income, and appreciation sits at the center of that argument.

Property appreciation, the standard industry term for real estate value growth over time, works because it compounds. A property worth $300,000 today at 4.5% annual growth reaches roughly $469,000 in ten years. That $169,000 gain requires no active management beyond holding the asset. For investors who buy property in 2025 and beyond, appreciation stacks on top of rental income and mortgage paydown to create three simultaneous wealth engines from a single purchase.

The leverage effect makes appreciation even more compelling. When you put $100,000 down on a $500,000 property, appreciation applies to the full property value, not just your initial capital. A 10% increase adds $50,000 to your net worth on a $100,000 investment. That is a 50% return on invested capital from appreciation alone, a ratio that most traditional asset classes cannot match.

Appreciation also interacts directly with equity. As the property value rises and the mortgage balance falls, your equity position accelerates. This equity can be accessed through a cash-out refinance to fund additional investments, creating a compounding cycle that experienced investors use deliberately and repeatedly.

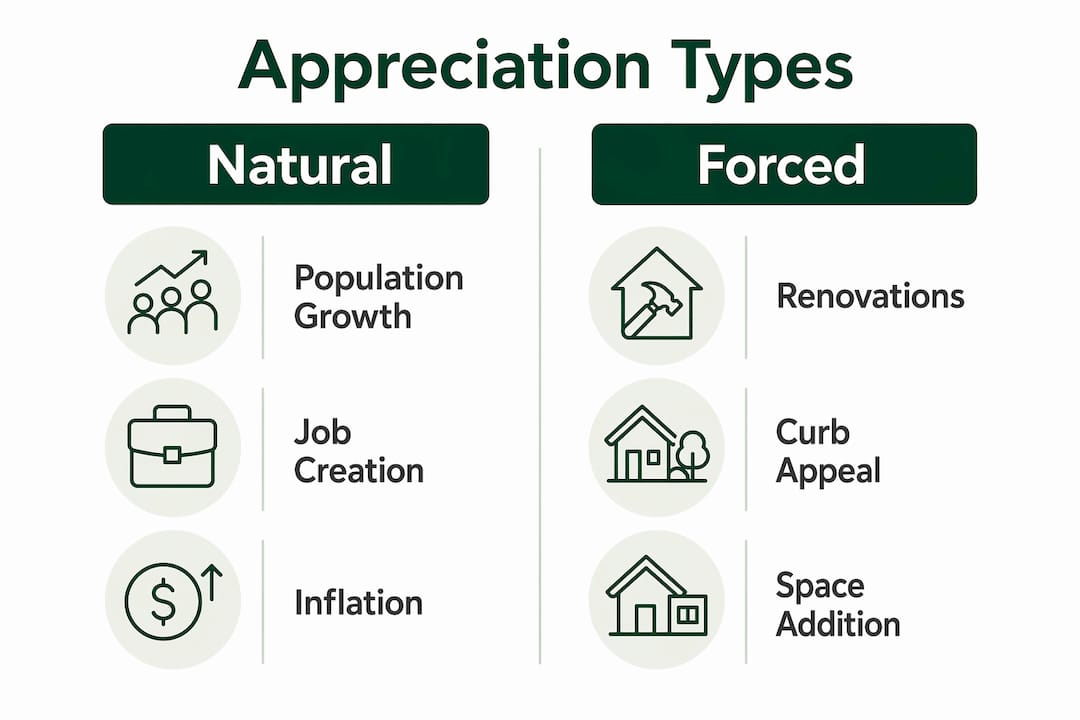

Appreciation does not happen randomly. Two categories of forces determine how fast and how reliably a property gains value.

Market-driven (natural) appreciation is passive. It is shaped by population growth, job creation, inflation, and supply constraints. When more people compete for a limited housing stock in a growing city, prices rise. Natural appreciation is driven by macro factors like population growth and jobs, and investors benefit from it simply by owning property in the right market.

Forced appreciation is owner-driven. Renovations, adding livable square footage, improving curb appeal, or increasing rental income on an investment property all push value upward independent of market conditions. Strategic upgrades can generate forced appreciation, though not all improvements yield equal returns. A kitchen remodel in a mid-range neighborhood delivers better ROI than a luxury pool in the same location.

Location remains the single most durable appreciation driver. School districts can increase home values by 49% over the national median, a figure that illustrates just how much buyers pay for access to quality education. Proximity to amenities matters too. 62% of buyers prioritize walkable neighborhoods, and 54% prioritize proximity to shopping and services, which sustains long-term demand and price growth. The role of location in Beit Shemesh follows the same logic: neighborhoods with strong community infrastructure and amenity access consistently outperform isolated developments.

| Appreciation driver | Investor control | Impact level |

|---|---|---|

| Local job market growth | None | High |

| School district quality | None | High |

| Walkability and amenities | Low | High |

| Property condition and upgrades | Full | Medium to high |

| Inflation | None | Medium |

| Supply constraints | None | High |

Pro Tip: Before purchasing, check the local market absorption rate. A rate under four months of inventory signals a seller’s market where natural appreciation is more likely to accelerate.

The financial benefits of appreciation extend well beyond a higher sale price. Here is how appreciation compounds returns across a typical investment timeline.

Pro Tip: Never underwrite a deal based solely on projected appreciation. Run the numbers assuming zero appreciation and confirm the property still generates positive cash flow. Appreciation should be a bonus, not a lifeline.

The impact of market trends on property values means that investors who understand local economic cycles capture appreciation more reliably than those who rely on national averages alone.

Appreciation is not guaranteed. Markets decline, stagnate, and correct. Treating appreciation as a certainty is the most common and costly mistake new investors make.

Real estate appreciation rewards patience and punishes speculation. The investors who hold quality assets in strong markets for 15 or 20 years consistently outperform those who chase short-term price movements.

Treating property as a long-term commitment rather than a trading vehicle is not just philosophical advice. It is the structural requirement for appreciation to deliver its full benefit.

Due diligence on appreciation potential requires looking beyond the listing price. The community factors surrounding a property, including employment growth, infrastructure investment, and neighborhood cohesion, are as important as the property itself.

Key due diligence areas:

For investors who want to actively create value, forced appreciation tactics offer a direct path. Renovating kitchens and bathrooms, converting unused space into livable square footage, and improving energy efficiency all add measurable value. For rental properties, increasing net operating income through better management or higher rents raises the property’s capitalized value directly.

Pro Tip: Before any renovation, get three contractor bids and compare the total cost against comparable sales data for upgraded properties in the same neighborhood. If the upgrade costs $40,000 and adds $35,000 in value, it destroys equity rather than creating it.

A disciplined approach to evaluating property listings combines market analysis with property-specific assessment to identify assets where both natural and forced appreciation are realistic outcomes.

Property appreciation builds wealth most effectively when investors combine location-driven natural appreciation with deliberate forced appreciation tactics over a holding period of at least ten years.

| Point | Details |

|---|---|

| Average annual appreciation | Homes have grown 4.5% per year since 2001, per the Zillow Home Value Index. |

| Leverage multiplies returns | Appreciation on the full asset value generates outsized returns relative to the down payment invested. |

| Real vs. nominal gains | Inflation-adjusted appreciation is closer to 3% annually; plan for purchasing power, not headline numbers. |

| Forced appreciation adds control | Strategic renovations and income improvements create value independent of market conditions. |

| Appreciation is not a substitute for cash flow | Every deal must work at current rents; appreciation is a bonus, not the investment thesis. |

The investors I respect most treat appreciation the way a good chef treats seasoning. It enhances the dish, but it is not the dish. The foundation of every sound real estate investment is a property that generates positive cash flow from day one, purchased at or below market value in a location with genuine demand drivers.

Where I see new investors go wrong is in building their entire financial case on optimistic appreciation forecasts. They buy a property that bleeds cash every month and tell themselves the appreciation will cover it. Sometimes it does. More often, a market correction or an unexpected repair bill forces a sale at the worst possible time, turning a paper gain into a real loss.

The most underrated appreciation strategy is patience combined with local knowledge. Markets like Beit Shemesh, where Yigal-realty operates, have structural demand drivers rooted in community growth, religious infrastructure, and limited supply. Those fundamentals do not disappear in a correction. They compress temporarily and then resume. Investors who understand those local dynamics hold through volatility instead of panic-selling, and they capture the full compounding benefit that appreciation offers over a 15 to 20 year horizon.

Forced appreciation deserves more attention than it gets. Buying a property with cosmetic problems in a strong neighborhood, improving it deliberately, and refinancing to capture the new equity is a repeatable system. It does not require a rising market. It requires skill, discipline, and a clear-eyed view of renovation costs versus value added.

Appreciation is real, it is powerful, and it is one of the best reasons to own property. Just never let it be the only reason.

— Spiros

Yigal-realty specializes in residential properties in Beit Shemesh and surrounding areas, with a focus on markets that carry genuine long-term appreciation drivers: community infrastructure, growing demand from observant families, and limited housing supply. Whether you are evaluating your first investment or expanding an existing portfolio, the team at Yigal-realty provides local market insight, project guidance, and access to developments before they reach the open market. Explore current listings and investment opportunities directly on the Yigal-realty platform, where you can connect with agents who understand both the financial and community dimensions of property value in this market.

Property appreciation in real estate is the increase in a property’s market value over time, driven by factors including location quality, local economic growth, supply constraints, and property improvements. The Zillow Home Value Index shows U.S. homes have appreciated at an average of 4.5% annually since 2001.

Appreciation increases an investor’s equity and net worth without requiring additional capital, and because it applies to the full property value rather than just the down payment, it multiplies returns on the initial investment through leverage.

Natural appreciation is passive and driven by market forces like job growth and population increases, while forced appreciation is owner-driven through renovations, added square footage, or improved rental income.

Appreciation is not guaranteed. Markets can decline during economic downturns, and nominal appreciation of 4.5% annually adjusts down to roughly 3% in real, inflation-adjusted terms. Investors should underwrite deals assuming zero appreciation and treat value growth as a secondary benefit.

Focus due diligence on school district quality, local employment trends, and neighborhood trajectory. Supplement natural appreciation with forced appreciation tactics like strategic renovations and income improvements, always verifying that upgrade costs are justified by comparable sales data in the same area.