%20(4).png)

![[background image] image of cityscape background (for an architect firm)](https://cdn.prod.website-files.com/68961ade6feff9cbdffc080d/69384e066e0e9a310b6817f8_061f6bac-48bf-44b8-a689-078dacd8009f.avif)

TL;DR:

- Despite slow but steady growth in 2025, buying now offers better mortgage rates, increased inventory, and bargaining power. Local market conditions and long-term wealth-building benefits outweigh waiting for price drops or market booms. Strategic negotiation and timely action are key to making advantageous real estate investments today.

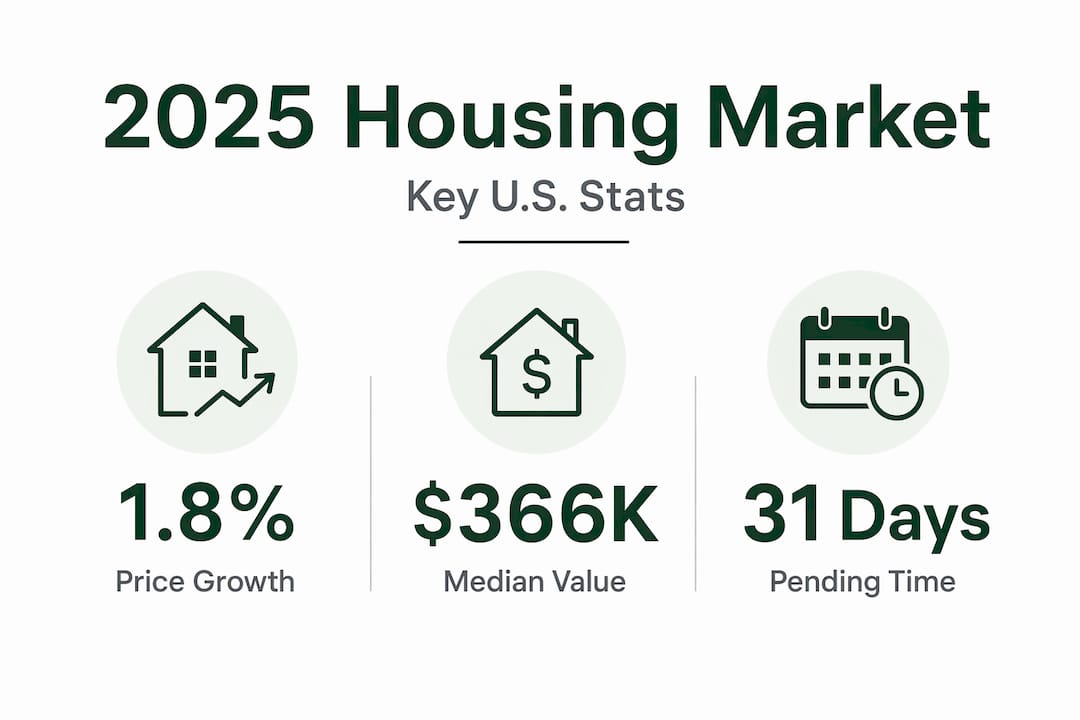

If you’re asking why buy property in 2025, you’re not alone, and the answer isn’t as simple as “prices are rising” or “rates are high.” The market is genuinely mixed. House prices rose 1.8% year over year through Q4 2025, showing steady but slower appreciation. At the same time, mortgage rates have eased, inventory has climbed, and buyers are finding more room to negotiate than they’ve had in years. For individuals and families ready to think long-term, the case for buying now is built on fundamentals, not speculation.

| Point | Details |

|---|---|

| Prices are still rising | National home values grew 1.8% in 2025, so waiting rarely means paying less. |

| Rates are near multi-year lows | Mortgage rates around 6% improve what you can qualify for today. |

| Inventory favors buyers | More listings mean more negotiating power on price, repairs, and closing costs. |

| Long-term value beats timing | Real estate builds wealth and diversifies your portfolio far better than short-term timing strategies. |

| Local data matters most | National averages don’t tell your story. Neighborhood-level trends decide real outcomes. |

The first thing to understand is that 2025 was not a crash and not a boom. It was a recalibration. Price growth continued nationally, but at a pace that gave buyers more breathing room than the frenzied years of 2020 to 2022.

| Metric | 2025 Data |

|---|---|

| National home price growth (YOY) | 1.8% (FHFA Q4 2025) |

| Average U.S. home value | $366,019 |

| Average days to pending sale | 31 days |

| Unsold inventory (March 2026) | 1.36 million units |

| First-time buyers (March 2026) | 32% of transactions |

| Cash buyers (March 2026) | 27% of transactions |

The average home value of $366,019 with homes going pending in 31 days shows a market that’s active but no longer frantic. That 31-day average is meaningful. In 2021, well-priced homes were getting multiple offers within 48 hours. Today’s pace gives you time to think, inspect, and negotiate.

Existing-home sales fell 3.6% month over month in March 2026, and with 1.36 million unsold units sitting on the market, sellers are competing for your attention. That’s a structural shift from where things were just two years ago. And with 32% of buyers being first-timers, there’s real diversity in who’s buying, which tells you the market isn’t just investors or cash-heavy purchasers locking out regular families.

The slowdown in sales volume does not signal a collapsing market. It signals a market where deliberate buyers, people like you, have regained leverage.

A lot of people fixate on home prices. Experienced buyers focus on monthly payments. That distinction matters more than most headlines acknowledge.

Mortgage rates dropped to 6.09% in early 2026, the lowest level in nearly four years. That shift has a direct impact on your purchasing power. Consider a $400,000 loan. At 7.5%, your principal and interest payment is roughly $2,797 per month. At 6.09%, that same loan costs about $2,426 per month. That’s $371 per month back in your pocket, which is more than $4,400 per year, without any change in home price.

Monthly payment modeling consistently shows that modest rate changes impact your qualification and affordability more than small swings in home prices. If you’ve been waiting for a 5% price drop, a rate increase of 0.5% would wipe out almost all of those savings.

Here’s what to act on in today’s rate environment:

Pro Tip: When comparing lenders, ask for a Loan Estimate within three days of application. Federal law requires it, and it gives you an apples-to-apples comparison of rates, fees, and total costs.

The core insight here is that affordability decisions should be driven by your personal finances and current rates, not by macro headlines about where prices might go in 18 months. Rates near a four-year low represent a real window.

One of the most overlooked reasons to buy in 2025 is what you can negotiate beyond the price. The conversation has shifted.

Redfin reports the strongest buyer’s market in years, with roughly 600,000 more sellers than buyers in the market at one point. When supply outpaces demand at that scale, sellers become cooperative in ways they weren’t during the competitive years. That cooperation shows up in more ways than a lower listing price.

Buyers are successfully negotiating:

Properties with longer days on market are particularly worth targeting. Targeting slower-moving listings and negotiating on terms rather than just price is one of the clearest strategies for winning in this market. A home sitting for 60 or 90 days without a contract is a seller who’s ready to talk.

Pro Tip: Before making an offer, research how long comparable homes in that zip code have been sitting on the market. If the average is 45 days and your target is at 70, you have a negotiating foundation. Bring that data to the table.

One critical caution: local market conditions drive outcomes more than national trends. A neighborhood where out-of-market demand remains high may still feel like a seller’s market even when the national data looks favorable for buyers. Check neighborhood-level days on market and active listings before assuming you have leverage. You can explore negotiation strategies for homebuyers in more detail if you want to prepare before approaching sellers.

The best reasons to buy in 2025 aren’t really about 2025. They’re about what owning real estate does for your financial life over the next 10, 20, and 30 years. Here are the four that matter most.

Portfolio diversification you can’t replicate another way. Private real estate shows low or negative correlation with stocks and bonds, meaning when markets drop, your property doesn’t necessarily follow. That behavior is rare among major asset classes and genuinely valuable for families building long-term wealth.

An inflation hedge with a practical floor. Real estate has historically retained purchasing power through inflationary cycles because both property values and rents tend to rise with inflation. If you own the asset, you benefit from that dynamic instead of watching your rent payment increase year after year.

Rental income potential. Even if you’re buying a primary residence, a second unit, an accessory dwelling, or a future investment purchase creates a recurring income stream. That income can cover part or all of your mortgage over time, changing the real cost of ownership significantly.

Structural demand shifts in select markets. 61.9% of online property views in the largest metros came from out-of-market shoppers in late 2025. That kind of cross-market demand signals lasting interest in specific areas, and properties in those corridors benefit from a buyer pool that isn’t dependent on local economic conditions alone.

The real estate investment advantages in 2025 extend well beyond what the price tag says today. Equity, tax benefits, housing stability, and generational wealth transfer are all part of the picture. Waiting for a “perfect” price means forfeiting years of those compounding benefits.

I’ve had a lot of conversations with buyers who said they were going to wait for prices to drop. In most cases, they waited, prices didn’t fall meaningfully, and then rates moved in the wrong direction. They ended up paying more per month on a home that cost the same or slightly less.

What I’ve learned is that the question should never be “will prices fall?” The question should be “can I afford this today, and am I buying a property with real fundamentals behind it?” Those are answerable questions. The first one is speculation.

In my experience, buyers who win in a slow market aren’t the ones who held out for a 10% price cut. They’re the ones who moved fast on a well-priced listing that had been sitting, negotiated aggressively on terms, and locked a rate before it ticked back up. That combination, the right property plus smart financing plus creative negotiation, is more powerful than any price drop you might hope for.

I also think people underestimate how much local knowledge changes outcomes. I’ve seen two buyers purchase in the same city in the same month. One bought in a neighborhood with rising out-of-market demand and sold two years later with strong appreciation. The other bought in a saturated submarket and saw flat values. National headlines told both of them the same thing. Local data told a completely different story.

The market in 2025 rewards prepared buyers. Get your finances in order, study the neighborhoods you care about at the street level, and negotiate like you know the data. Because now, you do.

— Spiros

Understanding why buy property in 2025 is one thing. Knowing which property, in which location, at which terms, is where expertise becomes the difference between a good decision and a great one.

Yigal-realty specializes in residential properties in Beit Shemesh and surrounding areas, with a specific focus on communities built for observant and religious families. Their team combines on-the-ground local knowledge with access to new project listings, off-market opportunities, and early-stage developments that don’t show up on general listing platforms. For international buyers, their New York office makes the process accessible without requiring you to navigate it entirely from overseas.

If you’re ready to move from evaluating to deciding, explore current real estate opportunities with Yigal-realty’s team to see what’s available right now. You can also review the 2025 property trends in Israel to understand how the Israeli market compares to the dynamics covered in this article. The 2025 market rewards buyers who act with the right information and the right team behind them.

Prices rose 1.8% through Q4 2025 and mortgage rates are near four-year lows, meaning waiting typically costs more in both appreciation missed and potentially higher future rates.

Most of the country is seeing buyer-friendly conditions, with inventory at its highest levels in years and roughly 600,000 more sellers than buyers according to Redfin data.

A 1% change in mortgage rates on a $400,000 loan shifts your monthly payment by roughly $200 to $250, which affects your qualification ceiling more than a small change in home price.

Local data is more predictive. Out-of-market demand, neighborhood days on market, and local inventory levels determine your actual buying conditions far better than national averages.

Seller credits for closing costs, repair credits, flexible contingency periods, and closing date flexibility are all legitimate negotiating points in today’s slower-moving market.