%20(4).png)

![[background image] image of cityscape background (for an architect firm)](https://cdn.prod.website-files.com/68961ade6feff9cbdffc080d/69384e066e0e9a310b6817f8_061f6bac-48bf-44b8-a689-078dacd8009f.avif)

TL;DR:

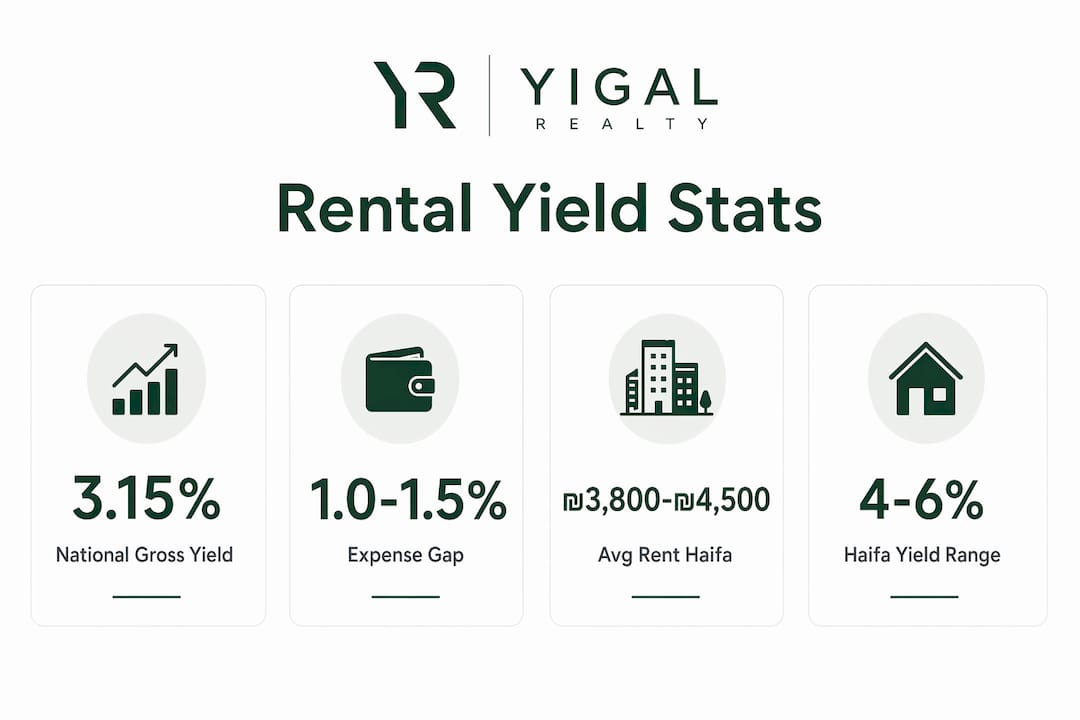

- Rental yield in Israel is primarily an appreciation story, with modest gross yields averaging around 3.15%.

- Investors must account for significant costs like vacancy, maintenance, taxes, and financing to determine true net yield, often reducing it by 1 to 1.5 percentage points.

Rental yield is defined as annual rental income divided by the property purchase price, expressed as a percentage. For anyone explaining rental yield in Israel, the critical starting point is this: Israel’s market is an appreciation story, not an income story. Gross yields average around 3.15% nationally, which is modest by global standards. Knowing how to read that number correctly, and what sits beneath it, separates investors who profit from those who are surprised by negative cash flow.

Rental yield is the industry-standard metric for measuring the income return on a property investment. The gross rental yield formula is straightforward: (Annual Rent ÷ Purchase Price) × 100. If you pay ₪1,500,000 for an apartment and collect ₪48,000 per year in rent, your gross yield is 3.2%.

That number, however, is only the starting point. Net yield falls 1.0–1.5 percentage points below gross once you subtract real operating expenses. In Israel, those expenses are specific and significant.

The gap between gross and net yield is where most first-time investors in Israel get caught off guard. A property that looks like a 3.5% gross yield can easily drop to 2.0% net once you account for all costs. Net yield is the only number that reflects what you actually keep.

Pro Tip: Always calculate net yield before you make an offer. If a seller or agent quotes only gross yield, ask them to itemize annual expenses. If they cannot, build your own estimate using the list above.

Location is the single biggest driver of yield variation in Israel. National gross yield averages 3.15%, but that figure masks a wide spread between cities. Haifa consistently delivers the highest yields, while Tel Aviv sits at the bottom of the range.

The table below summarizes current gross yield ranges and approximate average monthly rents by city.

| City | Gross Yield Range | Avg. Monthly Rent (2BR) | Risk Profile |

|---|---|---|---|

| Haifa | 4%–6% | ₪3,800–₪4,500 | Moderate |

| Ashdod / Ashkelon | 3.5%–5% | ₪4,000–₪4,800 | Low-Moderate |

| Beit Shemesh | 3.2%–3.8% | ₪4,200–₪5,000 | Low |

| Jerusalem | 3%–4% | ₪4,500–₪5,500 | Low-Moderate |

| Tel Aviv | 2.5%–3.5% | ₪5,500–₪7,500 | Low |

Higher yields in cities like Haifa and Ashdod reflect lower purchase prices relative to rent, not necessarily stronger rental demand. Average monthly rents nationally reached ₪4,550 for a two-bedroom as of early 2026, with 6% year-over-year growth. That rent growth is real, but it does not automatically translate into better yields if purchase prices are rising at the same pace.

Beit Shemesh occupies a strong middle position. It offers yields above Tel Aviv’s floor, a growing population base, and strong demand from religious and observant communities, which creates consistent tenant demand. For investors focused on yield and capital growth together, this balance matters.

Pro Tip: Do not chase a city’s reputation. Verify actual rental comps on current listings before you run any yield calculation. A neighborhood with strong university enrollment, a tech corridor, or a major transit hub will outperform a prestigious address with weak tenant demand.

This is where Israel’s property investment math gets uncomfortable. Fixed unindexed mortgage rates currently run 4.7%–5.0%, which often exceeds the net rental yield in prime markets. In Tel Aviv, net yields of 1.6%–1.9% against a 4.8% mortgage rate means you are paying more in interest than you are collecting in net rent. That is negative carry, and it is common.

Beyond the mortgage, investors face a layered set of transaction and holding costs:

The practical takeaway is this: a property with a 3.5% gross yield can deliver a negative cash-on-cash return once financing is factored in. Cash-on-cash return measures net income against actual cash invested, not just purchase price. For leveraged buyers, this is the number that tells the real story. Consult a mortgage adviser and a licensed Israeli lawyer before committing to any purchase.

Smart property investment in Israel starts with realistic assumptions, not optimistic ones. Stress-testing projections using current rents and a vacancy buffer is the baseline discipline every investor needs. Here is what that looks like in practice.

Pro Tip: Run your numbers at 90% occupancy, not 100%. If the investment still works at that occupancy rate, you have a defensible position. If it only works when fully occupied every month of the year, the risk is too high.

Understanding tax benefits for real estate in Israel can also shift the net yield picture. Structuring your rental income correctly under Israeli tax law is a legitimate way to improve after-tax returns without changing the property itself.

Rental yield in Israel rewards investors who calculate net returns carefully, account for all costs, and select properties based on real demand rather than reputation.

| Point | Details |

|---|---|

| Gross vs. net yield gap | Net yield runs 1.0–1.5 points below gross after expenses; always calculate net before buying. |

| City yield spread | Haifa yields 4%–6% gross; Tel Aviv yields 2.5%–3.5%; Beit Shemesh sits at 3.2%–3.8%. |

| Financing risk | Mortgage rates of 4.7%–5.0% often exceed net yields in prime markets, creating negative cash flow. |

| Transaction costs | Investor purchase tax of 8%–10% adds ₪160,000+ on a ₪2,000,000 property before you hold a key. |

| Smaller units win on net | Fixed costs like arnona and va’ad bayit hit smaller apartments proportionally less, improving net yield. |

I have watched investors walk into the Israeli market with a gross yield figure in hand and walk out confused about why the numbers stopped working six months later. Israel is not a cash-flow market. It never has been. The investors who do well here understand that from the start.

The mistake I see most often is treating gross yield as the investment thesis. Someone finds a 4.5% gross yield in Haifa, gets excited, and skips the net yield math. By the time you subtract vacancy, management fees, arnona during empty months, and the tax bill, that 4.5% can look a lot more like 2.8%. That is still a reasonable return in a market where capital appreciation has historically been strong. But it is a very different investment than the headline number suggested.

My honest read on Israel in 2026 is this: buy for appreciation with yield as a partial offset, not the primary return driver. The cities and neighborhoods that hold value and grow are the ones with real demand. Beit Shemesh is a good example. It has a growing population, a defined community base, and yields that sit above Tel Aviv’s floor without the speculative premium. That combination is more durable than chasing the highest gross yield number on a spreadsheet.

Do the full net yield calculation. Stress-test it at lower rents and higher vacancy. If the investment still makes sense, you have something worth pursuing.

— Spiros

Yigal-realty specializes in residential properties in Beit Shemesh and surrounding areas, with a client base that includes international investors who need clear, honest yield analysis before committing. The team at Yigal-realty understands the full cost picture: purchase tax, financing, local fees, and the rental demand drivers that make one building outperform another on the same street. If you are evaluating Israeli real estate and want property-specific yield projections grounded in real market data, explore current listings and investment options directly with the Yigal-realty team. They also operate a New York office for international clients who need guidance before traveling to Israel.

Rental yield is the annual rent a property generates divided by its purchase price, expressed as a percentage. A property bought for ₪1,500,000 that earns ₪48,000 per year has a gross rental yield of 3.2%.

A gross yield above 3.5% is considered solid in Israel, with net yields of 2.5%–3% representing a realistic target after expenses. Haifa and Ashdod consistently offer the strongest gross yields, ranging from 3.5%–6%.

Subtract annual expenses (vacancy, maintenance, management fees, arnona, and taxes) from annual rent, then divide by the purchase price and multiply by 100. Net yield typically runs 1.0–1.5 percentage points below gross yield in Israel.

Yes, significantly. Fixed unindexed mortgage rates of 4.7%–5.0% often exceed net rental yields in Tel Aviv and Jerusalem, creating negative monthly cash flow. Cash-on-cash return, which measures net income against actual cash invested, is the more accurate metric for leveraged buyers.

Smaller units generally deliver better net yields because fixed costs like arnona and building committee fees represent a smaller share of total rent collected. This makes studios and one-bedroom apartments more defensible income investments than larger luxury units.