%20(4).png)

![[background image] image of cityscape background (for an architect firm)](https://cdn.prod.website-files.com/68961ade6feff9cbdffc080d/69384e066e0e9a310b6817f8_061f6bac-48bf-44b8-a689-078dacd8009f.avif)

TL;DR:

- Analyzing the Israeli property market involves reviewing official transaction data, macroeconomic trends, and legal processes to make informed investment decisions.

- Market analysis must focus on actual sold prices, transaction volume, and local legal factors rather than relying solely on listing prices or macro trends.

Analyzing the Israeli property market means examining recorded transaction prices, macroeconomic trends, and local legal processes to make informed investment decisions. The Israeli real estate market operates differently from North American and European markets. It uses government portals, unique purchase contracts, and a legal framework that directly shapes pricing and risk. Whether you are a local buyer or an international investor, understanding these mechanics gives you a real edge. This guide walks you through the exact tools, data sources, and analytical steps you need.

The single most important step in any property market analysis in Israel is accessing actual sold prices, not listing prices. The Nadlan Gov portal, operated by the Israeli government, publishes recorded transaction data for residential properties across the country. This is your primary source of truth.

Here is how to use it effectively:

The Central Bureau of Statistics (CBS) publishes housing market snapshots that complement Nadlan Gov data. CBS figures give you macro indicators: national price trends, sales volume changes, and mortgage activity. Use Nadlan Gov for micro-level price verification and CBS for the broader picture.

Pro Tip: When using Nadlan Gov, always note the construction year of comparable sales. A 1990s building and a 2020 building in the same neighborhood can differ by 20–30% in price per square meter, even with similar room counts.

Understanding Israeli real estate requires tracking both price direction and transaction volume. Price alone tells an incomplete story.

| Indicator | What It Measures | Why It Matters |

|---|---|---|

| Sales volume (monthly) | Number of completed transactions | Low volume signals weak demand or buyer hesitation |

| Price change (period over period) | Percentage shift in average sold price | Reveals direction of market momentum |

| New-build inventory | Units available for sale from developers | High supply can suppress prices in specific submarkets |

| Mortgage interest rates | Cost of borrowing for buyers | Higher rates reduce purchasing power and slow sales |

| Shekel/USD exchange rate | Currency strength for overseas buyers | Strong shekel raises effective cost for dollar-based investors |

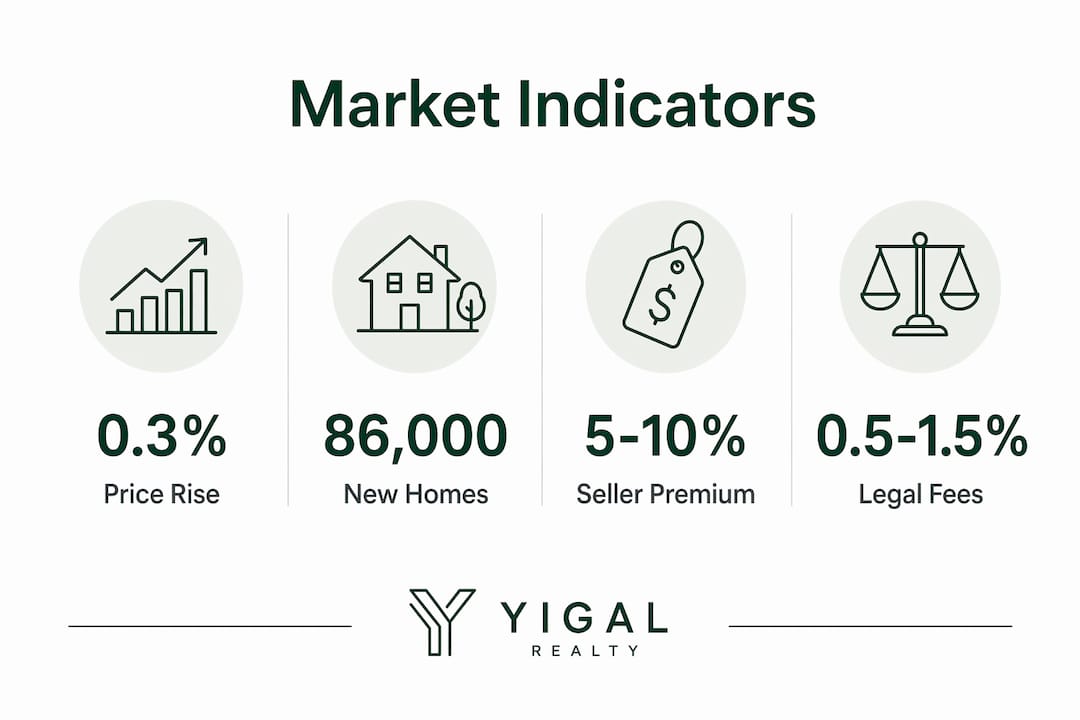

CBS data shows that home prices rose 0.3% in February and March 2026 compared to the prior period. At the same time, apartment sales in March 2026 were 8% lower than March 2025. That combination tells you prices are holding, but buyer activity is cooling. High interest rates and a strong shekel are the primary drivers of that slowdown.

For overseas investors, shekel strength matters directly. When the shekel appreciates against the dollar or euro, the same property costs more in foreign currency terms. Tracking the exchange rate over a 12-month window before committing to a purchase is standard practice for any serious international buyer.

Supply is another critical variable. A record 86,000 new homes were available for sale in 2026, creating supply pressure in certain submarkets. New-build inventory at that scale can soften prices in areas with concentrated development, even when national sentiment is positive. Always analyze the submarket, not just the national headline.

Pro Tip: Track sales volume month over month, not just year over year. A sudden drop in monthly transactions often precedes a price correction by 3–6 months. Volume leads price.

The Israeli residential purchase process differs significantly from what buyers in the United States or United Kingdom expect. Local legal frameworks and transaction timings require a tailored approach for foreign investors. Ignoring these differences leads to flawed investment models.

Here is the standard purchase sequence:

Two additional factors affect investment returns directly:

For a detailed breakdown of each transaction step, the Yigal-realty transaction guide covers legal fees, timelines, and documentation in plain language.

Raw listing data in Israel contains measurement inconsistencies that distort price-per-square-meter calculations. Correcting for these is not optional. It is the difference between an accurate analysis and a costly mistake.

Key normalization steps every buyer should follow:

Most analytical errors in the Israeli market come from one source: treating listing data as market data. The two are not the same.

Pro Tip: Always combine official data from Nadlan Gov and CBS with direct input from a local agent who specializes in your target submarket. Government data tells you what happened. A good local agent tells you what is happening right now.

Accurate Israeli property market analysis requires combining government transaction data, macroeconomic indicators, and local legal knowledge to build a reliable investment picture.

| Point | Details |

|---|---|

| Use Nadlan Gov for sold prices | Filter by property type, timeframe, and size to find true market value, not listing price. |

| Track volume alongside price | Declining transaction volume often signals a price correction before it appears in averages. |

| Model all transaction costs | Legal fees, purchase tax, and finishing costs can add 8–15% above the base purchase price. |

| Normalize square meter data | Verify usable space against official registry records to avoid overpaying on inflated measurements. |

| Analyze submarkets separately | National price trends mask local variation; always evaluate your specific neighborhood independently. |

I have seen buyers walk into the Israeli market with spreadsheets built entirely on Yad2 listing prices. They model their returns on those numbers, get excited, and then discover the actual sold prices are 8–10% lower. That gap does not sound dramatic until you are talking about a NIS 2,000,000 apartment. Suddenly you are off by NIS 160,000–200,000 in your base assumption, and the whole investment thesis shifts.

The other pattern I see constantly is foreign buyers underestimating finishing costs on shell apartments. They see a price that looks competitive, factor in legal fees, and think they have a complete picture. Then the finishing bill arrives and it is NIS 300,000 they did not plan for. That is not a rounding error. That is a material change to the investment.

What actually works is a two-layer approach. You use the official data portals to establish a price floor, then you use a local agent with real transaction history in that specific submarket to pressure-test your assumptions. The market shows genuine resilience. Prices held positive even through significant geopolitical pressure in early 2026. But resilience does not mean you can skip the analytical work. Patient buyers who do the homework consistently get better entry prices than those who move fast on incomplete data.

— Spiros

Yigal-realty specializes in residential properties in Beit Shemesh and surrounding areas, with direct support for both local buyers and international investors. Their team provides project-specific guidance, local market insight, and transparent breakdowns of legal fees and transaction timelines. For buyers who want to skip the guesswork on buying property in Israel, Yigal-realty offers personalized support from initial search through contract signing. They also maintain a New York office for overseas clients who need guidance before arriving in Israel. Visit the Yigal-realty property portal to explore current listings, development projects, and direct agent contact.

Nadlan Gov is Israel’s official government database of recorded residential property transactions. It publishes actual sold prices, not asking prices, making it the most reliable tool for property market analysis in Israel.

Legal fees for a residential purchase in Israel typically run 0.5%–1.5% of the purchase price. Buyers should also budget for purchase tax, agent commissions, and registration fees on top of that figure.

CBS data shows home prices rose 0.3% in February and March 2026, despite a geopolitical environment that included active conflict. Transaction volume fell 8% year over year in March 2026, signaling cautious buyer activity.

Listing platforms like Yad2 reflect seller expectations, which commonly run 5–10% above actual sold prices recorded in Nadlan Gov. Relying on listing prices without cross-referencing transaction data leads to overpaying.

A shell apartment is a new-build unit sold without interior finishing. The buyer is responsible for flooring, kitchen, bathrooms, and all fixtures. Finishing costs can add NIS 150,000–400,000 or more to the total purchase cost and must be included in any investment model.