%20(4).png)

![[background image] image of cityscape background (for an architect firm)](https://cdn.prod.website-files.com/68961ade6feff9cbdffc080d/69384e066e0e9a310b6817f8_061f6bac-48bf-44b8-a689-078dacd8009f.avif)

TL;DR:

- Israeli mortgages, called mashkantas, consist of multiple interest-tracking layers tailored to risk and stability. Buyers typically combine fixed, CPI-linked, prime-linked, and adjustable tracks to optimize costs and flexibility. Regulations limit loan-to-value ratios and down payments, with special programs for olim, religious families, and investors.

If you assume an Israeli mortgage works like a standard American or British home loan, you’re in for a surprise. The Israeli mortgage system, known as a mashkanta, is built on a layered structure of multiple loan tracks, each with its own interest mechanism and risk profile. Mortgages in Israel are structured as multiple tracks called maslulim, regulated tightly by the Bank of Israel. For families making aliyah, observant buyers, and international investors, this system offers real advantages, but only if you understand how it works before you sign anything.

| Point | Details |

|---|---|

| Israeli mortgages are multi-track | Your loan combines multiple interest types for balanced risk and regulation. |

| Special benefits for olim and families | New immigrants and families in religious communities may access subsidized tracks, higher LTV ratios, or community funding. |

| Regulations are strict | Loan limits, track rules, and approval ratios are tightly regulated for financial stability. |

| Brokers and strategy matter | Choosing the right mix of tracks and an experienced broker can save you money and smooth your home buying experience. |

The word mashkanta comes from the Aramaic root for collateral. In practice, it refers to a property loan issued by an Israeli bank or licensed lender, secured against the home being purchased. What sets it apart from most Western mortgage systems is that it is rarely a single loan with one interest rate. Instead, it is almost always a combination of several tracks, each behaving differently over time.

A mortgage in Israel is structured as multiple tracks called maslulim, each with distinct interest mechanisms. Think of it like a financial portfolio rather than a single product. Some tracks protect you from inflation. Others give you flexibility to pay off early. No single track does everything well, which is why the combination matters so much.

The Bank of Israel plays a central regulatory role. It sets rules on how much of your loan can be in variable tracks, what percentage of the property value you can borrow, and how long your loan term can run. These rules are not suggestions. Banks must follow them, and your mortgage advisor must work within them.

Here is a quick overview of how the mashkanta compares to a typical American mortgage:

| Feature | Israeli mashkanta | US mortgage |

|---|---|---|

| Loan structure | Multiple tracks (maslulim) | Single rate product |

| Inflation linkage | Yes, on CPI tracks | No |

| Max term | 30 years | 30 years |

| Regulator | Bank of Israel | CFPB / Fannie Mae |

| Down payment (first home) | 25% minimum | As low as 3.5% (FHA) |

Key features of the mashkanta include:

Pro Tip: Before you start comparing rates, review the real estate transaction steps in Israel so you know exactly when the mortgage application fits into the overall timeline.

With the basics clear, let’s see what specifically makes Israeli mortgages so distinctive.

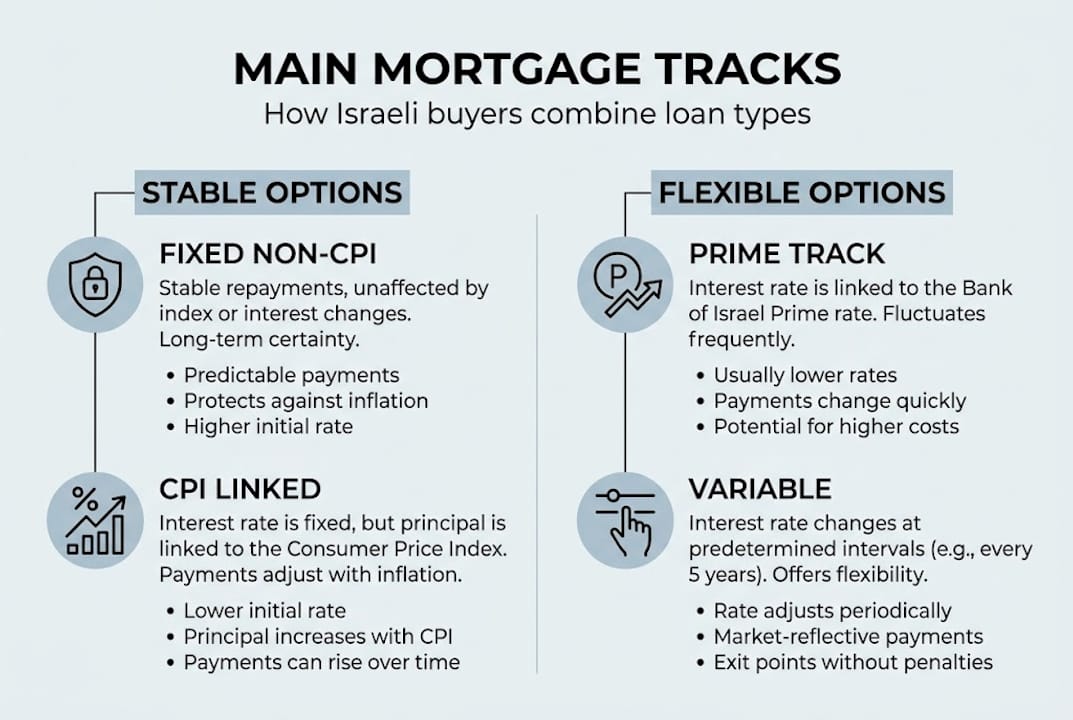

Once you understand the concept of tracks, it is crucial to grasp what types exist and how they are combined. The Bank of Israel permits several main track types, and most buyers end up using three or four of them together.

Main tracks include fixed non-CPI, CPI-linked fixed, prime-linked variable, and short-term adjustable, each with different rates and structures. Here is how each one works in practice:

In 2026, blended rates typically range from 4.2% to 4.8%, with fixed rates landing between 4.8% and 5.6%. Prime-linked tracks sit around 5.5%.

| Track type | Typical 2026 rate | Inflation risk | Prepayment flexibility |

|---|---|---|---|

| Fixed non-CPI | 4.8% to 5.6% | None | Low (penalties apply) |

| CPI-linked fixed | 2.5% to 3.5% real | High | Low |

| Prime-linked variable | ~5.5% | Moderate | High |

| Short-term adjustable | 4.2% to 4.8% | Moderate | Medium |

Most buyers combine tracks in roughly equal thirds: one third fixed non-CPI for stability, one third CPI-linked for lower base cost, and one third prime-linked for flexibility. This is not a rule but a common strategy.

Pro Tip: Explore your financing options for homebuyers before meeting with a bank. Knowing your options in advance puts you in a much stronger negotiating position.

Track choice can save or cost you hundreds of thousands of shekels over 25 to 30 years. Do not treat it as a minor detail.

Knowing how the tracks work, the next layer is understanding regulation, what the Bank of Israel allows and why. These rules exist to protect the financial system and, ultimately, you.

LTV is capped at 75% for a first home, 70% for replacements, and 50% for investment properties, with a maximum loan term of 30 years. That means if you are buying your first home in Israel for ₪2,000,000, the bank will lend you at most ₪1,500,000. You must bring the rest.

Key regulatory limits in 2026:

“The Bank of Israel’s mortgage regulations are designed not to frustrate buyers, but to prevent the kind of overleveraged household debt that caused financial crises in other countries.”

These rules have real consequences. If your income does not support the PTI threshold, you may need a co-borrower or a larger down payment. If you are buying an investment property, you need 50% cash upfront, which eliminates many casual investors from the market.

Refinancing is also regulated. Early exit from a fixed track triggers a penalty calculated on the interest rate differential. In a falling rate environment, this can actually work in your favor, but you need to calculate it carefully before acting. Review the steps to purchase process to understand where financing fits in the broader buying timeline.

For many readers, the standard tracks and regulations are just the starting point. Let’s see what special programs and community solutions exist.

Olim may qualify for 75% LTV, a subsidized Zakaut track up to ₪500,000 at roughly 3% to 3.5%, and reduced purchase tax. These benefits are significant. The Zakaut track alone can save tens of thousands of shekels compared to a standard bank rate, and the reduced purchase tax on a first property can be a major financial relief.

Benefits available to olim include:

Explore the financing paths for olim to see how these benefits layer together with standard mortgage tracks.

For observant and haredi buyers, the picture is more nuanced. Religious communities often use specialized brokers, interest-free loans known as GMAH, or parental funding for large purchases. In many cases, families pool resources across generations. A GMAH (gemach) loan from a community fund can cover a portion of the down payment interest-free, which is especially important for buyers who want to avoid interest-bearing debt for halachic reasons.

The observant buyer’s guide covers specific considerations for religious families navigating both the financial and halachic dimensions of property purchase.

For investors, the rules are stricter. The 50% LTV cap is firm, and rental income is only partially counted toward PTI calculations. Foreign non-residents face additional documentation requirements and are limited to 50% financing regardless of their financial profile.

Pro Tip: If you are an oleh or part of a religious community, work with a broker who has direct experience with these specific tracks and community resources. Generic bank advisors often miss benefits that specialists know well.

After laying out all the technical details, here is an honest look at what truly matters and what most people overlook.

Everyone obsesses over rates. Buyers spend hours comparing whether they can shave 0.1% off their prime track. But the mortgage acts as a risk portfolio, and a skilled broker can save you ₪50,000 or more simply by structuring the track mix correctly. The rate is almost secondary to the structure.

We have seen buyers lock into aggressive variable-heavy portfolios chasing low initial payments, only to face painful resets when prime rates moved. The regulation requiring at least one-third in fixed tracks exists precisely to prevent this. It is not red tape. It is a guardrail.

Community ties matter more than most guides admit. In Beit Shemesh and similar communities, experienced local brokers know which lenders are more flexible on documentation for olim, which GMAH funds are active, and which developers offer seller financing. That local knowledge is worth more than any rate comparison spreadsheet.

Our honest advice: prioritize predictability over optimization. A mortgage you can sleep with is worth more than one that looks great on paper but keeps you anxious every time the Bank of Israel meets. Review investment considerations if you are buying as an investor, because the calculus there is genuinely different.

You now have a solid foundation in how Israeli mortgages work, from track structures and regulatory limits to the special programs available for olim and observant families. But reading about mashkanta tracks is very different from navigating a live transaction with real deadlines and real money on the line.

Working with trusted advisors for Israeli real estate means you get professionals who understand both the financial and community dimensions of buying in Israel. Yigal Realty works with families, olim, and investors in Beit Shemesh and surrounding areas, offering bilingual support, local market knowledge, and connections to experienced mortgage advisors. Reach out to start a conversation before you begin your property search.

The minimum down payment is 25% for a first home, 30% for a replacement property, and 50% for an investment property, based on Bank of Israel LTV caps currently in effect.

Yes. Foreign non-residents are typically limited to 50% financing with stricter documentation, while olim can qualify for 75% LTV and access the subsidized Zakaut track.

Most buyers use a mix of fixed and variable tracks to spread risk. An optimal mix of roughly one-third per track is common, with olim and investors often weighting toward fixed tracks for predictability.

Yes. Religious communities use specialized brokers, interest-free GMAH loans from communal funds, and parental support alongside standard mortgage tracks to fund large purchases.

Yes. Refinancing is common when rates drop, though buyers should calculate prepayment penalties on fixed tracks before assuming refinancing will save money.